Analysis of Reddit Developer's One-Month Trading Framework: Technical Achievement vs. Trading Reality

解锁更多功能

登录后即可使用AI智能分析、深度投研报告等高级功能

关于我们:Ginlix AI 是由真实数据驱动的 AI 投资助手,将先进的人工智能与专业金融数据库相结合,提供可验证的、基于事实的答案。请使用下方的聊天框提出任何金融问题。

This analysis is based on a Reddit post [0] from November 7, 2025, where a software engineer with data/ML background seeks validation on building a complete trading framework within one month and whether it can generate consistent profits despite limited trading experience.

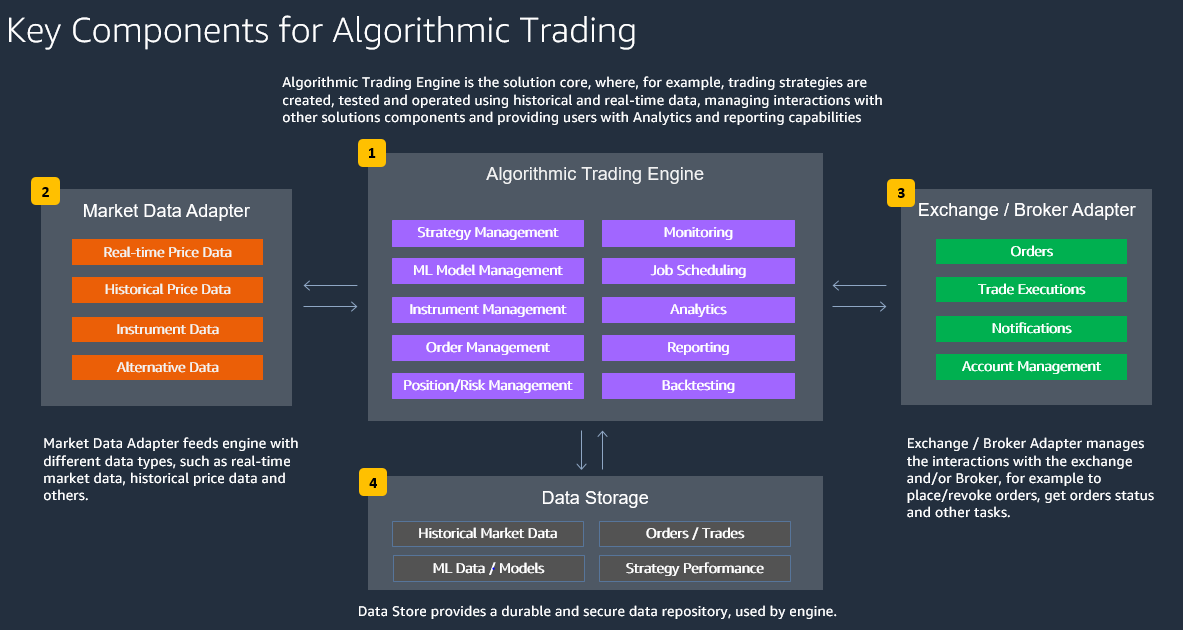

The developer’s accomplishment is technically remarkable, having built a comprehensive trading infrastructure including instruments management, portfolio management, JSON-based rule engine, backtester, and market simulator [0]. The system incorporates advanced features like decision tree rules, LLM-driven sentiment analysis, and plans for Keras models with evolutionary strategy optimization. This demonstrates strong software engineering capabilities and understanding of trading system architecture.

However, research indicates that the gap between building trading software and achieving profitable trading is substantial [3]. Successful quantitative trading typically requires deep understanding of market microstructure, transaction costs, slippage, and regime changes - knowledge that generally takes years to develop [3].

The algorithmic trading market is projected to grow from $18.02 billion in 2024 to $70.07 billion by 2035, representing a 13.14% CAGR [1]. Retail investors represent the fastest-growing segment at 12% annually [1], but face significant structural disadvantages:

- Institutional trading dominates with approximately 63% market share in 2024 [1]

- Retail traders have limited access to prime brokerage and optimal liquidity [4]

- Higher transaction costs and less favorable order routing impact profitability [4]

- Reduced access to exclusive market data and research [4]

The one-month timeline suggests potential overestimation of trading complexity [3]. While the technical framework appears comprehensive, successful algorithmic trading requires domain expertise that typically extends beyond software development skills. The retail algorithmic trading landscape is highly competitive, with major institutions like Goldman Sachs, Morgan Stanley, and JP Morgan maintaining dedicated quantitative research divisions with substantial resources [1].

Research on machine learning trading strategies shows mixed results. Some studies report success rates as high as 53.6% using convolutional neural networks [2], but these results often don’t account for real-world transaction costs, market impact, implementation delays, or regulatory constraints. Overfitting represents a major risk where models perform well on training data but fail to generalize to live markets [2].

Recent regulatory developments, such as SEBI’s framework for retail algorithmic trading in India, indicate increasing institutional acceptance and oversight [1]. Algorithm registration and approval requirements are becoming more common, adding complexity to retail trading operations.

- Overfitting Risk: Complex ML models with limited experience are prone to curve-fitting [2]

- Capital Risk: Real-money trading without sufficient backtesting and paper trading experience

- Technical Risk: Production trading systems require robust error handling, latency management, and fail-safes

- Market Structure Risk: Retail traders face significant disadvantages in execution quality and cost structure [4]

- Retail algorithmic traders have advantages in smaller markets where institutional funds cannot operate effectively [4]

- Democratization of trading technologies is creating new opportunities for sophisticated retail traders

- The growing market acceptance of algorithmic trading suggests expanding opportunities

- No backtesting results, Sharpe ratios, or maximum drawdown metrics provided [0]

- Limited discussion of position sizing, stop-loss mechanisms, or portfolio diversification

- Unclear market focus, timeframes, or instruments targeted

- No indication of account size or risk per trade parameters

The developer has created a technically sophisticated trading framework within one month, incorporating modern ML techniques and comprehensive system architecture. However, the path from technical implementation to consistent profitability in algorithmic trading typically requires extensive domain knowledge, rigorous validation, and substantial experience with market dynamics.

The current algorithmic trading environment is highly competitive, with retail traders facing structural disadvantages but also benefiting from growing market acceptance and technological democratization. Success requires addressing critical gaps in backtesting validation, risk management protocols, and real-world trading experience beyond the initial technical implementation.

Retail algorithmic traders should focus on smaller markets where institutional advantages are less pronounced, implement robust validation procedures to prevent overfitting, and develop comprehensive risk management systems before deploying capital. The technical foundation appears solid, but the trading expertise required for consistent profits typically extends well beyond the one-month development timeframe demonstrated.

数据基于历史,不代表未来趋势;仅供投资者参考,不构成投资建议

关于我们:Ginlix AI 是由真实数据驱动的 AI 投资助手,将先进的人工智能与专业金融数据库相结合,提供可验证的、基于事实的答案。请使用下方的聊天框提出任何金融问题。