POET Technologies: Photonics Play with Institutional Backing Faces High Valuation Risk

解锁更多功能

登录后即可使用AI智能分析、深度投研报告等高级功能

关于我们:Ginlix AI 是由真实数据驱动的 AI 投资助手,将先进的人工智能与专业金融数据库相结合,提供可验证的、基于事实的答案。请使用下方的聊天框提出任何金融问题。

相关个股

Reddit discussion highlights strong retail interest in POET’s options play, with 780k calls open interest and a low put-call ratio suggesting bullish sentiment. Many users express intent to buy Jan 2026/27 $10 calls, targeting $10-12 by year-end. However, sentiment is mixed - some users report bagholding at $9, while others caution about penny stock characteristics in company filings and repeated weekly DD posts. The community notes technical support at the lower band of an ascending channel but questions why the stock falls despite positive flow and gamma exposure.

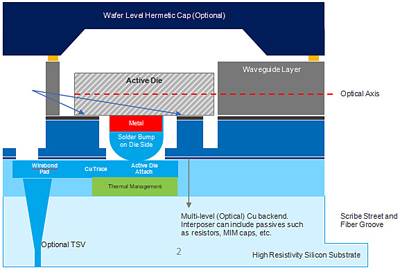

POET Technologies has secured significant institutional backing, closing a $150M registered direct offering on October 28, 2025, fully subscribed by two institutional investment managers. The company’s pro-forma cash position exceeded $300M post-offering. Strategic partnerships include Foxconn for 800G/1.6T transceiver modules, Semtech for 1.6T optical receivers (launched September 30, 2025), and Sivers Semiconductors for scalable laser modules. The company secured a $5M+ production order for 800G optical engines with H2 2026 deliveries. Total capital raised in 2025 exceeded $225M, including a $75M private placement.

The Reddit discussion appears to contain timing discrepancies - the $150M offering referenced actually occurred in October 2025, not 2024 as suggested in some posts. Both Reddit sentiment and research validate the strong institutional backing and strategic partnerships. However, research reveals significant valuation concerns that Reddit discussions may underemphasize - POET trades at approximately 30x projected 2026 revenues of ~$25M. While the strong cash buffer provides runway, the company remains unprofitable with minimal current revenue, facing competition from major chipmakers and alternative co-packaged optics solutions.

- Strong institutional validation with $300M+ cash position

- Strategic partnerships validate technology and market access

- AI data center growth driving demand for optical interconnect solutions

- First-mover advantage in silicon photonics optical interposers

- Extreme valuation multiple (~30x projected 2026 revenues)

- Minimal current revenue with unprofitable operations

- Competition from established semiconductor players

- Dependence on successful execution of H2 2026 production deliveries

- High retail speculation leading to potential volatility

数据基于历史,不代表未来趋势;仅供投资者参考,不构成投资建议

关于我们:Ginlix AI 是由真实数据驱动的 AI 投资助手,将先进的人工智能与专业金融数据库相结合,提供可验证的、基于事实的答案。请使用下方的聊天框提出任何金融问题。